Hydroxide Exchange Membrane Fuel Cell Technology in 2025: Unleashing Next-Gen Clean Energy Solutions and Market Acceleration. Explore the Innovations, Key Players, and Forecasts Shaping the Future of Sustainable Power.

- Executive Summary: 2025 Market Landscape and Key Takeaways

- Technology Overview: Principles and Recent Advances in Hydroxide Exchange Membrane Fuel Cells

- Competitive Benchmarking: Leading Companies and Industry Initiatives (e.g., ballard.com, toyota.com, plugpower.com)

- Market Size and Growth Forecasts: 2025–2030 (Estimated CAGR: 18–22%)

- Application Segments: Transportation, Stationary Power, and Emerging Uses

- Materials and Manufacturing Innovations: Membranes, Catalysts, and System Integration

- Policy, Regulation, and Industry Standards (e.g., fuelcellstandards.com, doe.gov)

- Investment Trends and Strategic Partnerships

- Challenges and Barriers: Technical, Economic, and Supply Chain Considerations

- Future Outlook: Disruptive Opportunities and Long-Term Impact on the Clean Energy Sector

- Sources & References

Executive Summary: 2025 Market Landscape and Key Takeaways

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is poised for significant advancements and market traction in 2025, driven by the global push for decarbonization, cost-effective hydrogen solutions, and the need for alternative fuel cell chemistries. HEMFCs, which operate using alkaline membranes, offer the potential for reduced reliance on precious metal catalysts and improved fuel flexibility compared to traditional proton exchange membrane (PEM) fuel cells. This positions HEMFCs as a promising candidate for both stationary and mobility applications in the evolving hydrogen economy.

In 2025, the HEMFC sector is characterized by a transition from laboratory-scale research to early-stage commercialization. Several industry leaders and technology developers are actively scaling up membrane production and integrating HEMFC stacks into demonstrator systems. DuPont, a global materials science company, continues to invest in advanced ionomer and membrane materials, supporting the development of robust and durable hydroxide exchange membranes. Toyota Motor Corporation and Honda Motor Co., Ltd.—both pioneers in fuel cell vehicle technology—are exploring HEMFCs as a pathway to reduce platinum group metal content and diversify their hydrogen vehicle portfolios.

European initiatives, such as those coordinated by Clean Hydrogen Partnership, are accelerating HEMFC research and demonstration projects, with a focus on heavy-duty transport and distributed power generation. The organization’s funding in 2025 is expected to support pilot deployments and the validation of HEMFC systems under real-world conditions. Meanwhile, Umicore, a leading materials and catalyst supplier, is expanding its portfolio to include non-precious metal catalysts tailored for alkaline environments, addressing a key cost barrier for HEMFC commercialization.

In Asia, Toray Industries, Inc. and Asahi Kasei Corporation are scaling up production of advanced polymer membranes and ionomers, aiming to supply the growing demand for HEMFC components. These companies are leveraging their expertise in polymer chemistry to enhance membrane conductivity and chemical stability, which are critical for long-term HEMFC operation.

Looking ahead, the outlook for HEMFC technology in the next few years is optimistic but contingent on continued material innovation, cost reduction, and system integration. Key takeaways for 2025 include:

- Increased investment from established chemical and automotive companies is accelerating the transition from R&D to early commercialization.

- Collaborative projects, especially in Europe and Asia, are validating HEMFC performance in transport and stationary applications.

- Material suppliers are focusing on scalable, durable, and cost-effective membrane and catalyst solutions to address technical bottlenecks.

- HEMFCs are emerging as a complementary technology to PEMFCs, with the potential to lower system costs and broaden the range of viable hydrogen sources.

Overall, 2025 marks a pivotal year for HEMFCs, with industry momentum building toward broader market adoption in the latter half of the decade.

Technology Overview: Principles and Recent Advances in Hydroxide Exchange Membrane Fuel Cells

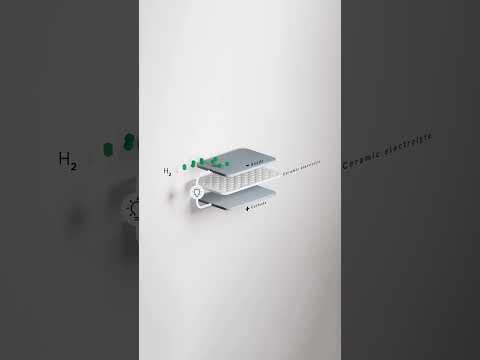

Hydroxide Exchange Membrane Fuel Cells (HEMFCs), also known as Anion Exchange Membrane Fuel Cells (AEMFCs), represent a rapidly advancing class of electrochemical energy conversion devices. Unlike Proton Exchange Membrane Fuel Cells (PEMFCs), HEMFCs operate by transporting hydroxide ions (OH−) from the cathode to the anode, enabling the use of non-precious metal catalysts and a broader range of fuels. This technology is gaining momentum in 2025 due to its potential for cost reduction, improved durability, and compatibility with sustainable hydrogen production.

The core of HEMFC technology is the hydroxide exchange membrane, which must exhibit high ionic conductivity, chemical stability in alkaline environments, and mechanical robustness. Recent years have seen significant advances in membrane materials, with companies such as 3M and DuPont developing new polymer chemistries that enhance conductivity and longevity. For instance, 3M’s research into quaternary ammonium-functionalized polymers has yielded membranes with improved alkaline stability, a critical factor for commercial viability.

Catalyst development is another area of rapid progress. The alkaline environment of HEMFCs allows for the use of non-platinum group metal (non-PGM) catalysts, which can significantly reduce system costs. Umicore, a global leader in catalyst technology, has been actively developing nickel-based and other non-PGM catalysts tailored for HEMFC applications. These innovations are expected to accelerate commercialization, as they address one of the main cost barriers associated with traditional PEMFCs.

System integration and stack design are also evolving. Ballard Power Systems, a prominent fuel cell manufacturer, has announced ongoing research into HEMFC stack architectures that optimize water management and gas diffusion, both of which are crucial for stable long-term operation. Their efforts are complemented by collaborations with automotive and stationary power companies aiming to deploy HEMFCs in real-world applications.

Looking ahead to the next few years, the outlook for HEMFC technology is promising. Industry roadmaps from organizations such as the Fuel Cell and Hydrogen Energy Association highlight HEMFCs as a key enabler for affordable, scalable hydrogen energy solutions. Demonstration projects in Europe, North America, and Asia are expected to validate performance targets and accelerate market entry. As material and manufacturing challenges are addressed, HEMFCs are poised to play a significant role in decarbonizing transportation, distributed power, and industrial sectors by the late 2020s.

Competitive Benchmarking: Leading Companies and Industry Initiatives (e.g., ballard.com, toyota.com, plugpower.com)

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is rapidly emerging as a promising alternative to traditional proton exchange membrane (PEM) fuel cells, primarily due to its potential for lower-cost catalysts and improved durability. As of 2025, the competitive landscape is shaped by a mix of established fuel cell manufacturers, automotive giants, and specialized membrane developers, each advancing HEMFC technology through R&D, pilot projects, and strategic partnerships.

Among the global leaders, Ballard Power Systems is recognized for its extensive fuel cell portfolio and ongoing research into next-generation membrane technologies. While Ballard’s commercial focus has historically centered on PEMFCs, the company has publicly acknowledged the potential of hydroxide exchange membranes and is investing in collaborative research to address challenges such as membrane stability and non-precious metal catalysts. Ballard’s partnerships with academic institutions and material suppliers are expected to yield demonstrator systems in the next few years.

Automotive manufacturers are also active in this space. Toyota Motor Corporation, a pioneer in hydrogen mobility, has signaled interest in HEMFCs as part of its broader hydrogen strategy. Toyota’s R&D divisions are exploring alternative membrane chemistries to reduce reliance on platinum group metals, aiming for cost-effective mass production. The company’s public statements and patent filings suggest that prototype vehicles or stationary systems utilizing HEMFCs could be unveiled before 2030, with incremental milestones anticipated by 2027.

In the United States, Plug Power Inc. is a key player in hydrogen fuel cell systems for material handling and stationary power. Plug Power has announced initiatives to diversify its membrane technology portfolio, including investments in hydroxide exchange membrane research. The company’s collaborations with membrane manufacturers and government-funded projects are expected to accelerate the commercialization timeline, with pilot deployments targeted for the latter half of the decade.

Specialized membrane developers such as 3M and DuPont are also instrumental in advancing HEMFC technology. Both companies are leveraging their expertise in polymer science to develop robust, high-conductivity hydroxide exchange membranes. Their materials are being tested in partnership with fuel cell integrators and automotive OEMs, with commercial-grade products anticipated to enter the market within the next few years.

Industry initiatives are further supported by organizations like the Fuel Cell and Hydrogen Energy Association, which coordinates collaborative research, standardization efforts, and policy advocacy. As HEMFC technology matures, competitive benchmarking will increasingly focus on system durability, cost per kilowatt, and scalability, with leading companies poised to announce significant technical milestones and commercial partnerships through 2025 and beyond.

Market Size and Growth Forecasts: 2025–2030 (Estimated CAGR: 18–22%)

The global market for Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is poised for robust expansion between 2025 and 2030, with industry consensus estimating a compound annual growth rate (CAGR) in the range of 18–22%. This surge is driven by increasing demand for clean energy solutions, advancements in membrane materials, and the growing adoption of fuel cells in transportation, stationary power, and portable applications.

HEMFCs, also known as Anion Exchange Membrane Fuel Cells (AEMFCs), offer several advantages over traditional Proton Exchange Membrane Fuel Cells (PEMFCs), including the use of non-precious metal catalysts and operation in alkaline environments, which can reduce system costs and improve sustainability. These attributes are attracting significant investment and R&D from both established players and emerging companies.

Key industry participants such as DuPont, a global leader in advanced materials, are actively developing next-generation hydroxide exchange membranes to enhance performance and durability. Toyota Motor Corporation continues to invest in fuel cell vehicle platforms, with ongoing research into alternative membrane chemistries, including HEMFCs, to diversify its zero-emission vehicle portfolio. Umicore, a major supplier of catalyst materials, is also expanding its product lines to support the shift toward non-platinum group metal catalysts compatible with HEMFCs.

In the Asia-Pacific region, Toray Industries and Asahi Kasei Corporation are scaling up production of advanced ion exchange membranes, targeting both domestic and international markets. These companies are leveraging their expertise in polymer chemistry to address the technical challenges of membrane stability and ionic conductivity, which are critical for commercial HEMFC deployment.

On the policy front, government initiatives in the European Union, United States, and China are accelerating the commercialization of HEMFC technology through funding programs, demonstration projects, and regulatory support for hydrogen infrastructure. Organizations such as the Fuel Cell and Hydrogen Energy Association are advocating for industry standards and public-private partnerships to facilitate market entry and scale-up.

Looking ahead to 2030, the HEMFC market is expected to benefit from continued cost reductions, improved membrane lifetimes, and the expansion of hydrogen supply chains. As the technology matures, it is anticipated that HEMFCs will capture a growing share of the fuel cell market, particularly in applications where cost and catalyst flexibility are paramount. The next five years will be pivotal in establishing HEMFCs as a mainstream clean energy solution.

Application Segments: Transportation, Stationary Power, and Emerging Uses

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is gaining momentum across multiple application segments, with 2025 marking a pivotal year for its commercial and pre-commercial deployments. HEMFCs, which operate using alkaline membranes, offer the promise of reduced reliance on precious metal catalysts and improved fuel flexibility compared to traditional proton exchange membrane (PEM) fuel cells. This is driving interest in transportation, stationary power, and emerging niche applications.

In the transportation sector, HEMFCs are being explored as a next-generation alternative for both light-duty and heavy-duty vehicles. Several automotive manufacturers and suppliers are actively developing HEMFC stacks and systems, aiming to leverage the technology’s potential for lower cost and higher efficiency. Toyota Motor Corporation and Honda Motor Co., Ltd.—both leaders in fuel cell vehicle (FCV) development—have signaled ongoing research into alkaline membrane systems, although commercial vehicles remain dominated by PEMFCs as of 2025. Meanwhile, Cummins Inc. and Ballard Power Systems are evaluating HEMFCs for commercial vehicle and bus applications, with pilot projects expected to expand in the next few years as membrane durability and catalyst performance improve.

For stationary power generation, HEMFCs are being positioned as a cost-effective solution for distributed and backup power, particularly where hydrogen or ammonia can be sourced locally. Companies such as Doosan Corporation and Bloom Energy are monitoring HEMFC advancements, with the latter’s solid oxide fuel cell (SOFC) expertise providing a potential pathway for hybrid systems. Demonstration projects in Asia and Europe are expected to scale up in 2025–2027, focusing on microgrid integration and renewable energy storage.

Emerging uses of HEMFCs include portable power, marine propulsion, and off-grid applications. The technology’s ability to utilize a wider range of fuels—including ammonia and alcohols—makes it attractive for sectors where hydrogen logistics are challenging. Nel ASA, a major hydrogen solutions provider, is collaborating with partners to develop HEMFC-compatible refueling infrastructure, while Air Liquide is supporting pilot deployments in maritime and remote energy systems.

Looking ahead, the outlook for HEMFC technology in 2025 and beyond is shaped by ongoing material innovations, cost reduction efforts, and the expansion of hydrogen supply chains. As leading industry players and new entrants accelerate R&D and demonstration activities, HEMFCs are poised to complement existing fuel cell technologies across diverse application segments, with commercial breakthroughs anticipated as technical barriers are addressed.

Materials and Manufacturing Innovations: Membranes, Catalysts, and System Integration

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is rapidly advancing, driven by the need for cost-effective, platinum-group-metal (PGM)-free alternatives to traditional proton exchange membrane fuel cells (PEMFCs). In 2025 and the coming years, significant progress is expected in materials, manufacturing, and system integration, with a focus on improving membrane durability, catalyst performance, and scalable production.

A central innovation in HEMFCs is the development of robust hydroxide exchange membranes (HEMs) that can operate stably under alkaline conditions. Recent efforts have focused on poly(aryl piperidinium) and poly(phenylene oxide)-based membranes, which offer improved chemical stability and ionic conductivity. Companies such as 3M and DuPont are actively developing advanced ionomer materials, leveraging their expertise in polymer chemistry to enhance membrane performance and longevity. These new membranes are designed to withstand the harsh alkaline environment and repeated hydration-dehydration cycles, a key challenge for commercial deployment.

Catalyst innovation is another critical area. HEMFCs enable the use of non-PGM catalysts, such as nickel, cobalt, and iron-based materials, which are more abundant and less expensive than platinum. Umicore, a global leader in catalyst technology, is investing in the development of high-activity, durable non-PGM catalysts tailored for alkaline environments. These efforts are complemented by research into catalyst layer architectures that maximize active surface area and facilitate efficient water management, both crucial for high power density and long-term operation.

Manufacturing scalability is being addressed through roll-to-roll processing and automated assembly lines, which are being adopted by membrane and MEA (membrane electrode assembly) producers. Ballard Power Systems and Advent Technologies are notable for their investments in scaling up HEMFC component production, aiming to reduce costs and meet the anticipated demand from transportation and stationary power sectors. These companies are also working on system integration, optimizing stack design and balance-of-plant components to ensure reliable, efficient operation in real-world applications.

Looking ahead, the outlook for HEMFC technology in 2025 and beyond is promising. Industry collaborations, such as those fostered by Hydrogen Europe, are accelerating the commercialization pathway by aligning material innovation with system-level requirements. As membrane and catalyst lifetimes improve and manufacturing costs decrease, HEMFCs are expected to become increasingly competitive for a range of applications, from light-duty vehicles to distributed energy systems.

Policy, Regulation, and Industry Standards (e.g., fuelcellstandards.com, doe.gov)

Policy, regulation, and industry standards are pivotal in shaping the development and commercialization of Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology. As of 2025, the global regulatory landscape is evolving to support the deployment of advanced fuel cell systems, including HEMFCs, which are recognized for their potential to enable cost-effective, platinum group metal (PGM)-free, and sustainable hydrogen energy solutions.

In the United States, the U.S. Department of Energy (DOE) continues to play a central role in setting research priorities and funding initiatives for HEMFCs. The DOE’s Hydrogen and Fuel Cell Technologies Office (HFTO) has established technical targets for fuel cell performance, durability, and cost, which directly influence HEMFC R&D. In 2024–2025, the DOE is emphasizing the development of PGM-free catalysts and membranes with high chemical stability in alkaline environments, aligning with HEMFC’s unique requirements. The DOE also supports the harmonization of testing protocols and pre-normative research to facilitate future standardization.

Internationally, the International Organization for Standardization (ISO) and the International Electrotechnical Commission (IEC) are actively updating standards relevant to fuel cell technologies. ISO 14687, which specifies hydrogen fuel quality, and IEC 62282, which covers safety and performance for fuel cell technologies, are being reviewed to ensure compatibility with emerging HEMFC systems. These standards are critical for ensuring interoperability, safety, and market acceptance.

Industry consortia and technical committees, such as those coordinated by the SAE International and the Fuel Cell Standards initiative, are working to address gaps in test methods and certification for hydroxide exchange membrane materials and stacks. In 2025, these groups are expected to release updated guidelines for accelerated stress testing, durability assessment, and system integration, reflecting the unique degradation mechanisms of HEMFCs.

On the policy front, several governments are incorporating HEMFCs into national hydrogen strategies. The European Union’s Clean Hydrogen Partnership, supported by the European Commission, is funding demonstration projects and pre-commercial deployments of HEMFCs, with a focus on heavy-duty transport and stationary power. Regulatory frameworks are being adapted to recognize the distinct characteristics of HEMFCs, such as their ability to use non-precious metal catalysts and operate at lower temperatures.

Looking ahead, the next few years will see increased alignment between regulatory agencies, standards bodies, and industry stakeholders to accelerate HEMFC commercialization. The establishment of universally accepted performance and safety standards, coupled with supportive policy incentives, is expected to lower barriers for market entry and foster global supply chain development for HEMFC components and systems.

Investment Trends and Strategic Partnerships

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is gaining momentum as a promising alternative to traditional proton exchange membrane fuel cells, particularly due to its potential for lower-cost catalysts and operation in alkaline environments. In 2025, investment trends and strategic partnerships are increasingly shaping the commercial landscape, with a focus on scaling up production, improving membrane durability, and integrating HEMFCs into diverse applications such as transportation, stationary power, and portable devices.

Several major chemical and energy companies are actively investing in HEMFC research and commercialization. DuPont, a global leader in advanced materials, continues to develop and supply ion exchange membranes, including those suitable for alkaline fuel cells. Their ongoing R&D efforts are supported by collaborations with fuel cell system integrators and automotive OEMs. Similarly, Umicore, known for its expertise in catalyst technologies, is expanding its portfolio to include non-platinum group metal catalysts tailored for HEMFCs, aiming to reduce system costs and improve sustainability.

Strategic partnerships are also emerging between membrane developers and fuel cell stack manufacturers. Toyota Motor Corporation has signaled interest in alkaline membrane fuel cells as part of its broader hydrogen strategy, leveraging its experience in fuel cell electric vehicles (FCEVs) to explore next-generation membrane technologies. In Europe, John Cockerill is collaborating with research institutes and startups to accelerate the deployment of HEMFC systems for industrial and grid applications.

Government-backed initiatives and consortia are playing a pivotal role in fostering innovation and de-risking investments. The European Union’s Clean Hydrogen Partnership, which includes participation from companies like BASF and Air Liquide, is funding projects aimed at improving membrane performance and scaling up manufacturing. These efforts are complemented by national programs in the United States, Japan, and China, where public-private partnerships are supporting pilot deployments and supply chain development.

Looking ahead to the next few years, the outlook for HEMFC technology is marked by increasing cross-sector collaboration. As automotive, chemical, and energy companies align their strategies, the sector is expected to see further capital inflows, joint ventures, and technology licensing agreements. The convergence of material innovation, manufacturing scale-up, and end-user engagement is likely to accelerate commercialization, positioning HEMFCs as a viable component of the global hydrogen economy by the late 2020s.

Challenges and Barriers: Technical, Economic, and Supply Chain Considerations

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is gaining attention as a promising alternative to traditional proton exchange membrane fuel cells (PEMFCs), particularly due to its potential for using non-precious metal catalysts and operation in alkaline environments. However, as of 2025, several technical, economic, and supply chain challenges continue to impede large-scale commercialization and deployment.

Technical Challenges remain at the forefront. The chemical stability and durability of hydroxide exchange membranes (HEMs) under real-world operating conditions are still under active investigation. Many HEMs suffer from degradation when exposed to high pH and elevated temperatures, leading to reduced lifetimes and performance losses. Additionally, while HEMFCs allow for the use of non-platinum group metal (non-PGM) catalysts, these alternatives often exhibit lower activity and stability compared to their precious metal counterparts. Companies such as 3M and DuPont are actively developing advanced membrane materials, but achieving the necessary balance between ionic conductivity, mechanical strength, and chemical resilience remains a significant hurdle.

Economic Barriers are closely tied to the technical limitations. Although HEMFCs promise cost reductions by enabling non-PGM catalysts, the current generation of membranes and ionomers are expensive to produce at scale. Manufacturing processes for high-performance HEMs are not yet fully optimized, and economies of scale have not been realized. Furthermore, the lack of standardized components and system architectures increases costs for system integrators and end-users. Major suppliers such as Toyochem and Asahi Kasei are investing in scaling up production, but widespread cost parity with PEMFCs is not expected in the immediate future.

Supply Chain Considerations are increasingly relevant as the industry looks to scale. The supply of high-purity ionomers, specialty polymers, and advanced catalysts is limited to a handful of manufacturers, creating potential bottlenecks. For example, Umicore and BASF are among the few global suppliers of advanced catalyst materials, and any disruption in their supply chains could impact the broader HEMFC market. Additionally, the geographic concentration of key raw material suppliers raises concerns about resilience and security, especially in light of recent global logistics disruptions.

Looking ahead to the next few years, industry stakeholders are focusing on collaborative R&D, standardization, and supply chain diversification to address these barriers. While technical breakthroughs in membrane chemistry and catalyst design are anticipated, the pace of progress will depend on sustained investment and cross-sector partnerships. The outlook for HEMFC technology in 2025 and beyond is cautiously optimistic, with incremental advances expected rather than rapid, transformative change.

Future Outlook: Disruptive Opportunities and Long-Term Impact on the Clean Energy Sector

Hydroxide Exchange Membrane Fuel Cell (HEMFC) technology is poised to play a transformative role in the clean energy sector over the coming years, with 2025 marking a pivotal period for both technological maturation and market entry. HEMFCs, which operate using alkaline membranes, offer the promise of reduced reliance on precious metal catalysts, lower operating temperatures, and compatibility with a broader range of fuels compared to traditional proton exchange membrane (PEM) fuel cells. These advantages position HEMFCs as a disruptive force, particularly in applications where cost and material sustainability are critical.

Several industry leaders and innovators are actively advancing HEMFC technology. Toyota Motor Corporation has publicly committed to expanding its fuel cell vehicle portfolio, and while its current models primarily use PEM technology, the company is investing in next-generation membrane research, including hydroxide exchange systems, to further reduce costs and improve performance. Similarly, Nel ASA, a global hydrogen solutions provider, is exploring integration of advanced membrane technologies to enhance the efficiency and scalability of hydrogen production and utilization, which directly supports the deployment of HEMFCs in both mobility and stationary power sectors.

In the United States, Ballard Power Systems is recognized for its leadership in fuel cell stack development and has ongoing research collaborations focused on alkaline and hydroxide exchange membranes. The company’s roadmap includes the commercialization of new membrane materials that could significantly lower the total cost of ownership for fuel cell systems by 2025 and beyond. Meanwhile, Umicore, a major supplier of fuel cell catalysts and materials, is investing in non-platinum group metal (PGM) catalyst development, which is particularly relevant for HEMFCs due to their compatibility with less expensive catalysts.

Looking ahead, the next few years are expected to see pilot deployments of HEMFCs in heavy-duty transport, distributed power generation, and backup power systems. The European Union’s continued funding for hydrogen and fuel cell innovation, through initiatives such as the Clean Hydrogen Partnership, is accelerating the commercialization timeline. Industry analysts anticipate that by 2027, HEMFCs could achieve cost parity with incumbent PEM systems in select markets, driven by advances in membrane durability, catalyst utilization, and system integration.

The long-term impact of HEMFC technology on the clean energy sector could be profound. By enabling more sustainable, cost-effective, and versatile fuel cell solutions, HEMFCs are likely to catalyze broader adoption of hydrogen as a clean energy vector, supporting decarbonization goals across transportation, industry, and grid applications.

Sources & References

- DuPont

- Toyota Motor Corporation

- Umicore

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Ballard Power Systems

- Doosan Corporation

- Bloom Energy

- Nel ASA

- Air Liquide

- Advent Technologies

- International Organization for Standardization

- European Commission

- BASF